Did you know? If you’re new to the world of credit, consider the

2-2-2 rule. Lenders want to see two forms of resolving credit (ie:

credit cards) with limits no less than $2,000 and a clean payment

history for two years.

Mortgage Tips Mohamed Mahmoud 31 Aug

Did you know? If you’re new to the world of credit, consider the

2-2-2 rule. Lenders want to see two forms of resolving credit (ie:

credit cards) with limits no less than $2,000 and a clean payment

history for two years.

FAQs Mohamed Mahmoud 27 Aug

You could get a lower interest rate, consolidate your debt, change your term or get a different mortgage or tap into your home equity to finance those renovations you’ve been dreaming about.

Mortgage Topics Mohamed Mahmoud 26 Aug

Most First Time Home Buyers are aware of down payment costs, but are not aware of closing costs. These are costs that go towards your legal fees, title insurance, and a few other costs that amount to anywhere between 1-4% of the purchase price of your new home.

It is worth noting that when applying for a Mortgage, most lenders require that you show proof of at least 1.5% of the purchase price, even though you might end up paying less than that amount!

For example, 1.5% of a $500,000 home is $7,500. This is what the lender would want to see as closing costs over and above the down payment funds. You might end up paying a total of $5,000 in closing costs, yet the lender would still need to see $7,500 as proof of closing costs.

General Mohamed Mahmoud 24 Aug

Life happens to families. If one income in the family is hindered not only does the family suffer but so can your mortgage. Protect your estate, your assets and your family and take a moment to hear about mortgage insurance.

If you think mortgage protection is too expensive, think again!

Mortgage insurance is vital to protecting yourself against loss of income due to disability or death of a borrower.

FAQs Mohamed Mahmoud 20 Aug

Great question!

1) It’s important to know that you can only tap into 80% of the value of your home.

2) You will need to pay a prepayment penalty, discharge, and legal fees, as this is considered a new Mortgage, and you will need to requalify for that Mortgage.

3 You can use a refinance to reduce payments, reduce interest costs, pay debts, renovate, and my personal favorite, purchase an investment property!

Dr. Sherry Cooper Mohamed Mahmoud 19 Aug

Canadian

Canadian

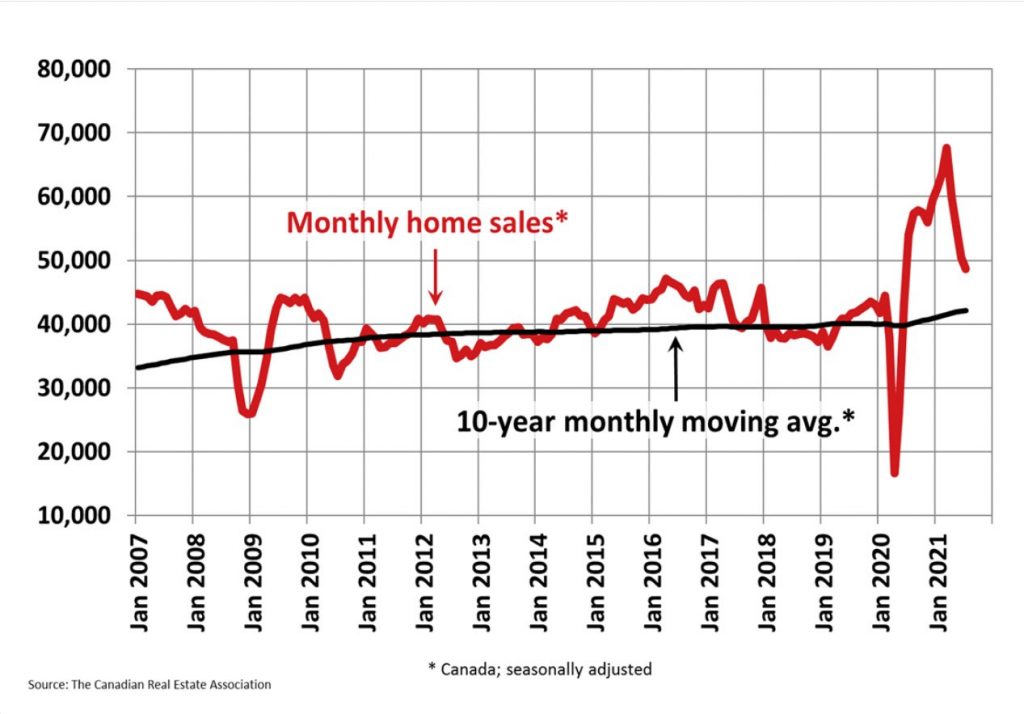

Existing home sales fell 3.5% on a month-over-month basis in July, marking the smallest of the four consecutive declines since March.

The Slowdown In Canadian Housing Continued in July

Today the Canadian Real Estate Association (CREA) released statistics showing national existing home sales fell 3.5% nationally from June to July 2021–the fourth consecutive monthly decline. Over the same period, the number of newly listed properties dropped 8.8%, and the MLS Home Price Index rose 0.6% and was up 22.2% year-over-year.

While sales are now down a cumulative 28% from the March peak, Canadian housing markets are still historically quite active (see Chart below). In July, the decline in sales activity was not as widespread geographically as in prior months, although sales were down in roughly two-thirds of all local markets. Edmonton and Calgary led the slowdown, but these cities didn’t experience falling sales until recently. In Montreal, in contrast, where sales began to moderate at the start of the year, activity edged up in July.

The actual (not seasonally adjusted) number of transactions in July 2021 was down 15.2% on a year-over-year basis from the record for that month set last July. July 2021 sales nonetheless still marked the second-best month of July on record.

“While the moderation of sales activity continues to capture most of the headlines these days, it’s record-low inventories that should be our focus,” said Cliff Stevenson, Chair of CREA. Most markets are in sellers’ market territory.

New Listings

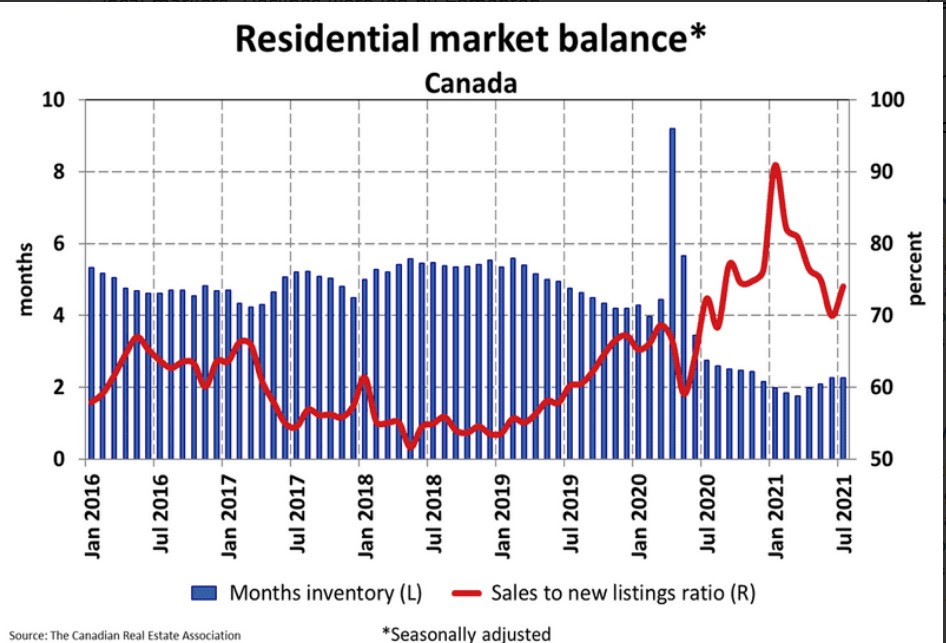

The number of newly listed homes dropped by 8.8% in July compared to June, with declines led by Canada’s largest cities – the GTA, Montreal, Vancouver and Calgary. Across the country, new supply was down in about three-quarters of all markets in July.

This was enough to noticeably tighten the sales-to-new listings ratio despite sales activity also slowing on the month. The national sales-to-new listings ratio was 74% in July 2021, up from 69.9% in June. The long-term average for the national sales-to-new listings ratio is 54.7%.

Based on a comparison of sales-to-new listings ratio with long-term averages, the tightening of market conditions in July tipped a small majority of local markets back into seller’s market territory, reversing the trend of more balanced markets seen in June.

Another piece of evidence that conditions may be starting to stabilize was the number of months of inventory. There were 2.3 months of inventory on a national basis at the end of July 2021, unchanged from June. This is extremely low – still indicative of a strong seller’s market at the national level and most local markets. The long-term average for this measure is twice where it stands today.

Home Prices

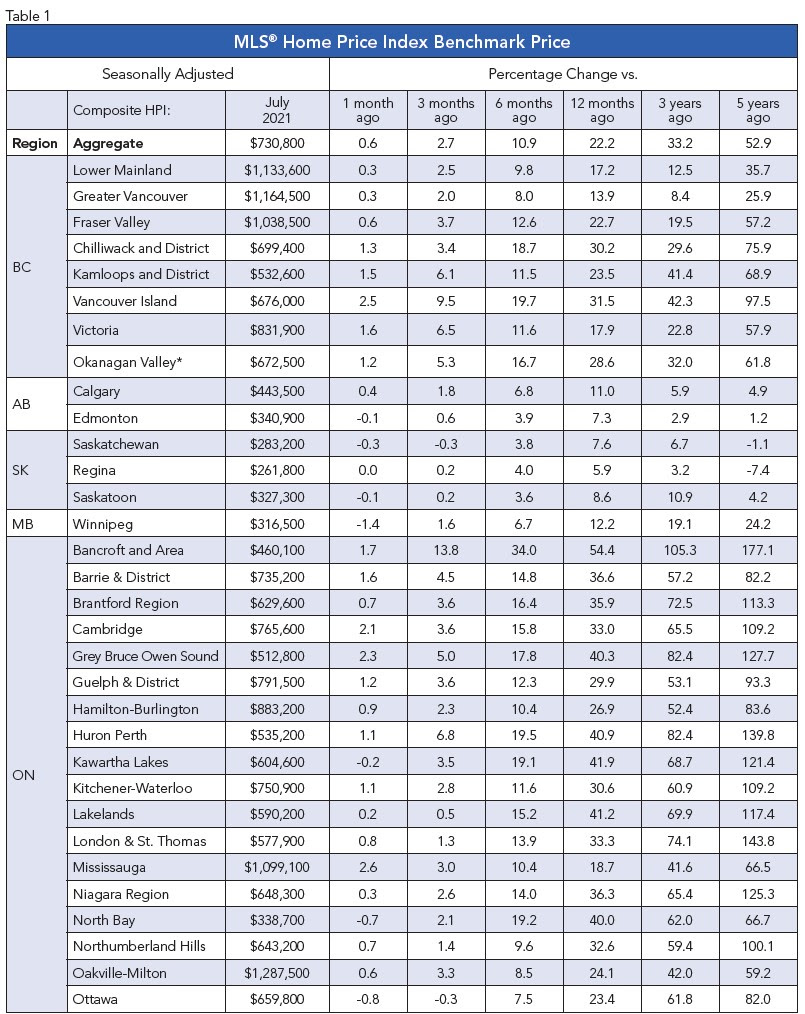

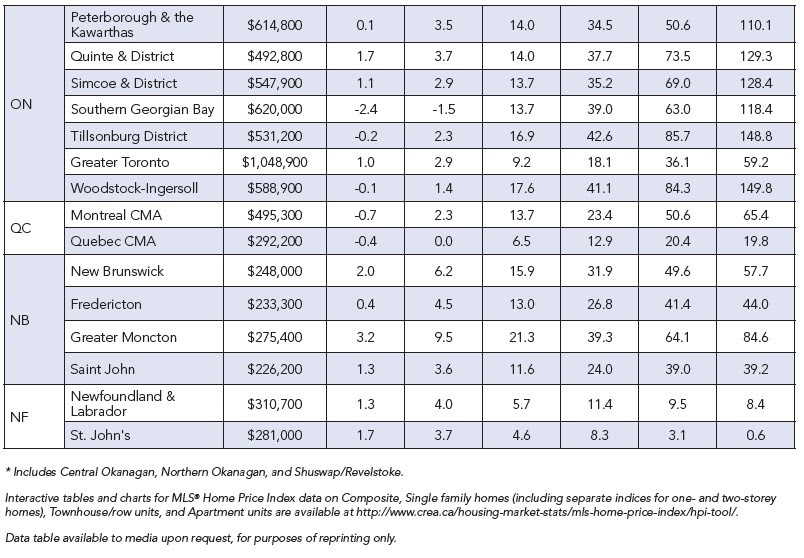

The Aggregate Composite MLS® Home Price Index (MLS® HPI) rose 0.6% month-over-month in July 2021, continuing the trend of decelerating month-over-month growth that began in March. That deceleration has yet to show up in any noticeable way on the East Coast, where property is relatively more affordable.

Additionally, a more recent point worth noting (and watching) just in the last month has seen prices for certain property types in certain Ontario markets look like they might be re-accelerating. This could be in line with a re-tightening of market conditions in some areas.

The non-seasonally adjusted Aggregate Composite MLS® HPI was up 22.2% on a year-over-year basis in July. While still a substantial gain, it was, as expected, down from the record 24.4% year-over-year increase in June. The reason the year-over-year comparison has started to fall is that we are now more than a year removed from when prices really took off last year, so last year’s price levels are now catching up with this year’s, even though prices are currently still rising from month to month.

Looking across the country, year-over-year price growth averages around 20% in B.C., though it is lower in Vancouver and higher in other parts of the province. Year-over-year price gains in the 10% range were recorded in Alberta and Saskatchewan, while gains are closer to 15% in Manitoba. Ontario sees an average year-over-year rate of price growth in the 30% range. However, as with B.C., gains are notably lower in the GTA and considerably higher in most other parts of the province. The opposite is true in Quebec, where Montreal is in the 25% range, and Quebec City is in the 15% range. Price growth is running a little above 30% in New Brunswick, while Newfoundland and Labrador is in the 10% range.

Bottom Line

Sales activity will continue to gradually cool over the next year, but it will take higher interest rates to soften the housing market in a meaningful way. Local housing markets are cooling off as prospective buyers contend with a dearth of houses for sale. Though increasing vaccination rates have begun to bring a return to normal life in Canada, that’s left the country to contend with one of the developed world’s most severe housing shortages and little prospect of much new supply becoming available soon.

Dr. Sherry Cooper

Chief Economist, Dominion Lending Centres

drcooper@dominionlending.ca

Mortgage Tips Mohamed Mahmoud 17 Aug

Strata Management is KEY for the long term investment of a strata property. Elect a good council and be involved! Read the minutes, attend the meetings and give a voice. Don’t cheap out on future planning!

If you’re purchasing a condo or townhouse within a strata you will have certain coverage under the strata but need to make sure you have personal condo insurance to cover any gaps!

FAQs Mohamed Mahmoud 13 Aug

Yes, your borrowing power is increased with a higher credit score, and in many cases most lenders offer better products and rates.

Generally, a score more than 680 is desirable to get the best options. Any score lower than that would a case by case scenario depending on the lender and strength of borrower. It’s also not just the score that counts. The details inside your credit report are just as important!

Call/Email to learn more

647 901 7948

info@modomortgages.ca

Mortgage Topics Mohamed Mahmoud 12 Aug

When talking budget, it is important to consider the purchase price budget, as well as your cash flow budget. Being house rich and cash poor makes for a no-fun home! The home price based on your cash flow budget may be dramatically different than the budget home price you qualify for.

The benefit of a budget is two-fold. Not only does it help you to understand your purchase price range and help you to find an affordable home, but it can also help you to see any gaps in your budget or opportunities for future savings. This will be instrumental when you become responsible for mortgage payments.

To help determine your budget, I suggest clicking here to download My Mortgage Toolbox app. This handy, consumer-friendly tool will help you determine your mortgage payments, affordability, income required to qualify and even the closing costs!

FAQs Mohamed Mahmoud 6 Aug

A fixed rate means you are locked in for a term (usually 5 years) and know your monthly mortgage payment.

Variable rates are often lower than a fixed rate and fluctuate with the Bank Of Canada posted rate. However, there are lenders that offer variable rates with stable monthly payments, which means you get the best of both worlds!

Call/Email me to learn more

(647) 901-7948

info@modomortgages.ca